Dresden at a glance

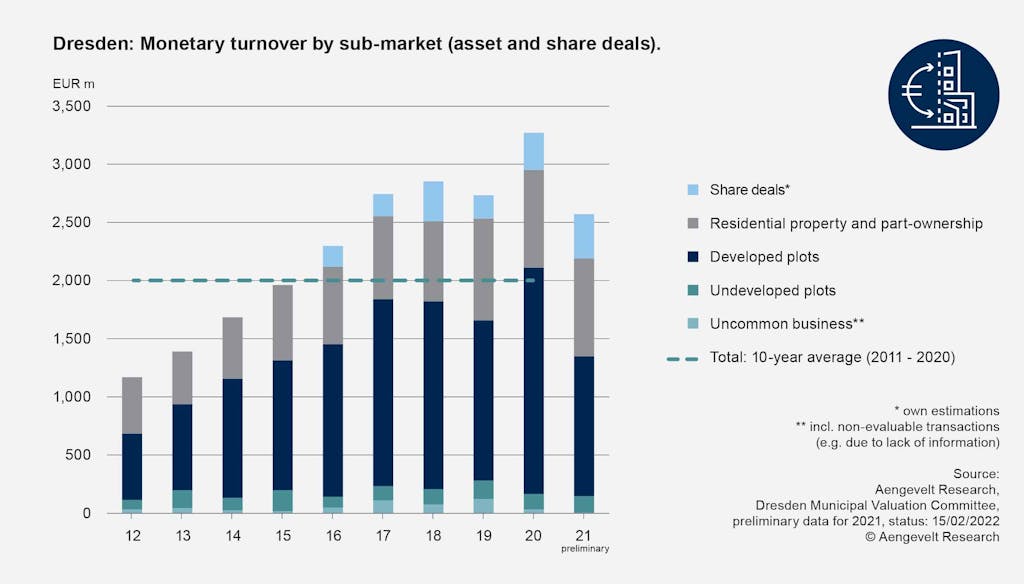

Dresden: Financial turnover by submarket (asset & share deals).

In the reporting year 2022, the transaction volume of all land and real estate traded in Dresden amounted to approximately EUR 2.19 billion (asset deals including transactions of unusual business transactions), thus the result from the previous year was repeated almost exactly (2021: EUR 2.19 billion). This year's result was only around 0.1% or EUR 3 million higher. In a ten-year comparison (average 2012 - 2021: EUR 2.11 billion), the result is around 3.9% or EUR 83 million above the average. In addition to conventional market activities, there are also share deals with a transaction volume of around EUR 320 million (2021: EUR 380 million), which has fallen by around EUR 60 million or 15.8% within a year. Total sales in the reporting year thus amount to around EUR 2.51 billion (2021: EUR 2.57 billion).

The transaction volume on the market for developed land (properties) increased by 20.7% in 2022 compared with the previous year and, according to preliminary analyses by the Dresden Valuation Committee, reached a value of EUR 1.45 billion. The monetary turnover thus exceeded the ten-year average by 16.1% (average 2012 - 2021: EUR 1.25 billion).

In particular, trading in land for residential and commercial properties (-79.5%), commercial properties (-62.9%) and undeveloped land for detached and semi-detached houses (-45.3%) decreased significantly compared to the previous year. With the exception of commercial properties, a decline was registered in all submarkets.

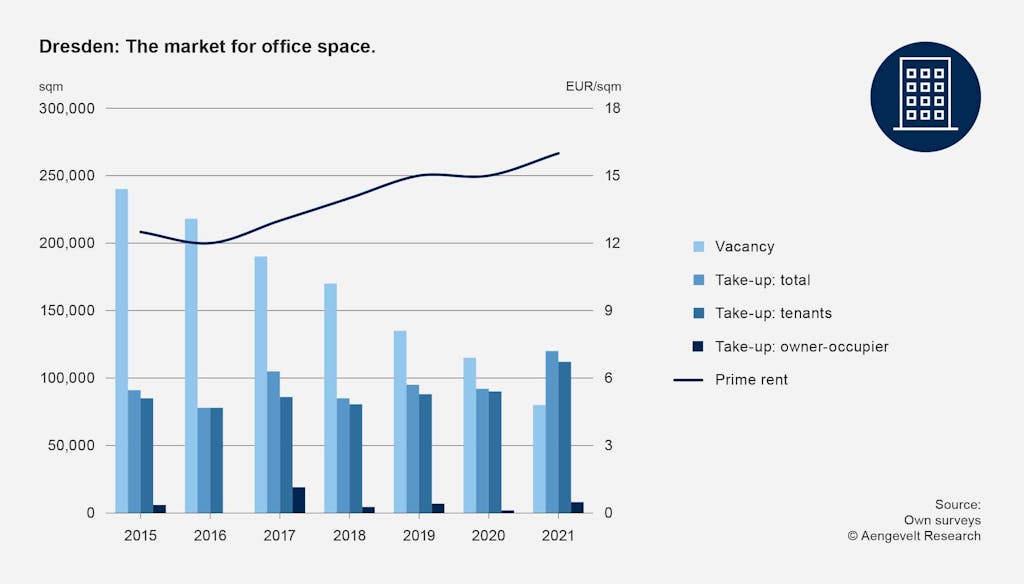

Dresden: The market for office space.

The Dresden office market achieved a comparatively moderate take-up of around 85,000 m² in 2022. The previous year's result (2021: 120,000 m²) was thus undercut by around 29.2% within a year, as was the ten-year average by around 8.3%. An analysis of take-up by size class shows an above-average take-up result in the small and medium-sized space segments in 2022. This means that the trend towards larger transactions seen in recent years did not continue in the year under review. For example, larger spaces are predominantly sought by the public sector.

In the top segment of the office space market, top rents (median of the 3-5% most expensive rental space) continued to rise. At EUR 18.50/m², the top rent is still well above the decade average of EUR 13.30/m².

Median rents in city center locations have risen to a current EUR 15.00/m². The adjacent city periphery is also showing a positive trend for new leases and will average EUR 12.00/m² in 2022 (2021: around EUR 11.00/m²).

The vacancy rate remained almost constant in the reporting year and only increased slightly. At the end of 2022, the vacancy rate will be around 90,000 m² or 3.5% of the portfolio of around 2.6 million m².

In the year under review, 68,300 m² of office space was completed, more than twice as much as in the previous year. The level is thus once again significantly higher than that of the past decade (average 2012 - 2021: 21,000 m²).

Dresden: Monetary turnover on the residential real estate market (asset deals).

According to preliminary evaluations by the GAA Dresden, the transaction volume on the overall residential market in Dresden (undeveloped, developed, residential and part-owned) amounted to around EUR 1.34 billion. This was around 2.9% down on the previous year (2021: EUR 1.38 billion), but around 14.5% above the long-term average (Ø 2012 - 2021: around EUR 1.17 billion).

The rental price range for reletting existing apartments was between EUR 6.70/m² and EUR 11.70/m² in 2022. On average, rents for existing apartments rose from EUR 8.20/m² in the previous year to EUR 8.40/m².

Rents for new apartments also continued to rise moderately. Here, an average of EUR 11.60/m² is paid for new leases. Rents of EUR 9.30/m² to EUR 15.90/m² are currently being demanded.

For all new residential construction (residential and non-residential), only around 1,512 (2021: 2,875) building permits were issued in the reporting year. Compared with the long-term ten-year average (2012 - 2021: 2,799 units), this represents a marked decline of 46.0%.

The housing market in the Saxon state capital is characterized by constant population growth, which is also reflected in rising rental and purchase prices in view of the shortage of housing, contributing to growing tension.

Ullrich Müller

Branch Manager Dresden

-

Salomonstraße 21 Brockhaus-Zentrum | 04103 Leipzig

- +49 341 99776-47

- u.mueller@aengevelt.com